How Insurance Claims Work in New Jersey: A Step-by-Step Guide for Property Owner

Introduction

New Jersey property owners face a complex and often frustrating landscape when navigating insurance claims. Whether caused by a burst pipe, kitchen fire, or storm-related roof failure, the claims process involves strict policy requirements, carrier-driven timelines, and a burden of documentation that falls heavily on the insured.

This article outlines the full insurance claim lifecycle in New Jersey—from the moment damage is discovered to the issuance of final payment. It is intended to serve as a foundational resource for homeowners, contractors, and professionals working in the insurance space.

1. Understanding Policy Coverage and Exclusions

Every claim starts with the policy. In New Jersey, homeowners policies are typically written on standardized forms (e.g., HO-3 or HO-5), but the actual scope of coverage depends on the endorsements, limits, and exclusions attached to that policy.

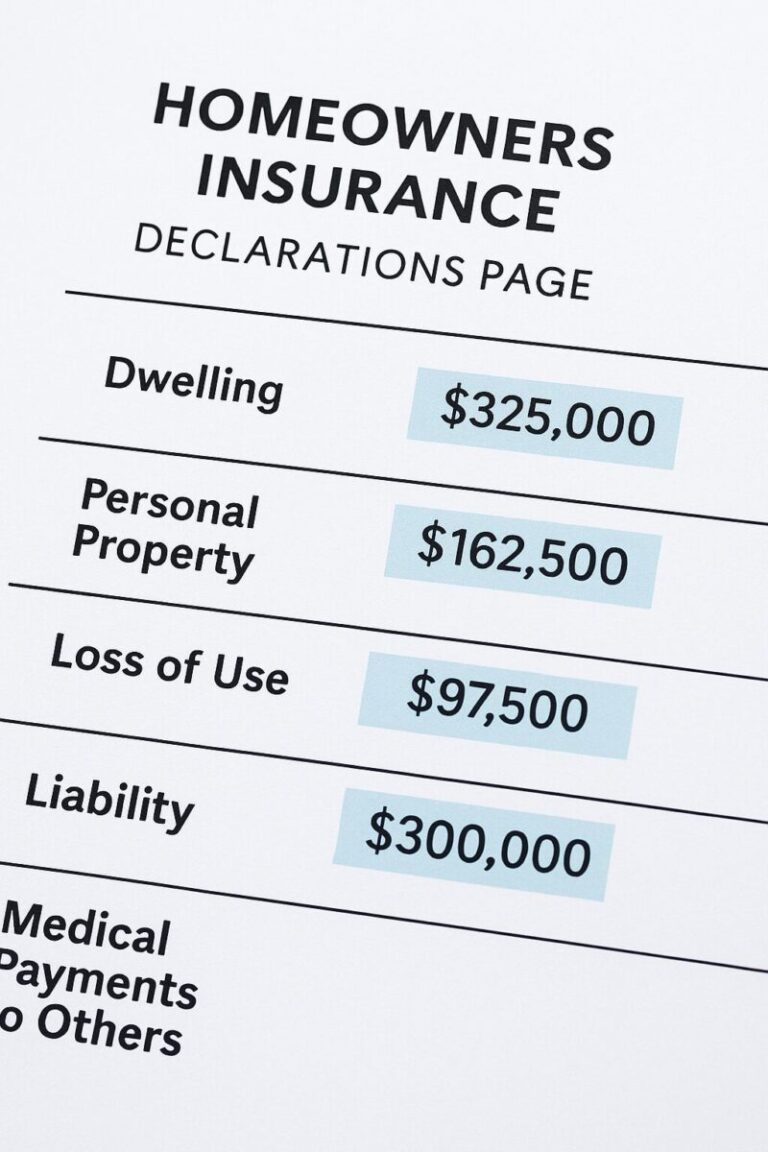

Key coverages include:

- Dwelling Coverage (Coverage A): Repairs to the home’s structure

- Other Structures (Coverage B): Sheds, garages, and fences

- Personal Property (Coverage C): Contents within the home

- Loss of Use (Coverage D): Reimbursement for temporary living expenses

- Liability Coverage (Coverage E): Legal protection for injury or property damage

Common exclusions in NJ policies:

- Flood damage (requires separate NFIP policy)

- Sewer and drain backup (typically needs endorsement)

- Earth movement, neglect, and long-term deterioration

- Mold, unless directly resulting from a covered peril

2. Initial Steps After Discovering Damage

The insured has a legal obligation to mitigate damage and notify their carrier “promptly.” While most policies do not define an exact timeframe, delays can be used as grounds for denial.

Immediate steps include:

- Photographing and filming all damage

- Retaining damaged items where safe to do so

- Notifying your carrier in writing (email suffices)

- Hiring emergency services (e.g., water mitigation, board-up)

Carriers often require you to use “reasonable means” to protect property from further damage. Inaction can trigger denial under the “neglect” exclusion.

3. The Carrier Assigns an Adjuster

Once the claim is initiated, the insurance company will assign an adjuster—either staff or independent—to inspect the property. This adjuster is tasked with evaluating the loss and producing an estimate based on the policy’s terms.

Note: The carrier’s adjuster represents the interests of the insurance company—not the policyholder.

In New Jersey, homeowners may also retain a licensed public adjuster, who advocates for the insured’s position and may submit a separate estimate or challenge inaccuracies in the insurer’s scope of work.

4. Estimating the Loss: Xactimate and Scope

The majority of property insurance estimates in NJ are written using Xactimate, a carrier-preferred software that calculates costs based on local pricing data.

However, estimates generated by carriers may:

- Understate material and labor costs

- Omit required building code upgrades

- Ignore indirect or latent damage

- Depreciate items improperly (e.g., roof depreciation without RCV endorsement)

New Jersey’s Uniform Construction Code (UCC) must be considered in any repair scope. Municipal inspectors may require full-code compliance—even if the insurance carrier attempts to cover only “like kind and quality.”

5. The Settlement Process

Once the adjuster submits their estimate, the carrier issues a determination of coverage. This will include:

- Scope of work with line-item pricing

- Coverage decisions (e.g., what is and isn’t covered)

- Deductible application

- Depreciation (ACV vs. RCV calculation)

- Payment structure (e.g., holdback on RCV)

Carriers may issue payments in stages:

- ACV Check: Paid up front based on depreciated value

- RCV Holdback: Paid upon completion of repairs

- ALE Reimbursements: Based on submitted receipts

Policyholders have the right to dispute any portion of this determination. In fact, under New Jersey law, carriers are required to handle claims fairly and promptly under the Unfair Claims Settlement Practices Act (N.J.A.C. 11:2-17).

6. Disputes, Appraisals, and Supplements

If the policyholder disagrees with the carrier’s findings, several options exist:

- Requesting a reinspection

- Submitting a competing estimate

- Invoking the appraisal clause (if included in the policy)

- Filing a supplement if additional damage is discovered

- Escalating to the NJ Department of Banking and Insurance

Supplements are particularly common in water and fire losses where hidden damage is only revealed after demolition. Contractors and public adjusters in New Jersey routinely submit supplements with additional evidence such as photos, expert reports, and building code citations.

7. Final Payment and Mortgage Involvement

Most carriers issue claim checks that include the mortgagee as a named payee. This means the check must be endorsed by your lender, and often deposited into a loss draft department account. This process can delay access to funds and requires submitting contractor bids and inspection reports to the mortgage company.

8. Post-Claim Considerations

After the claim is closed:

- Retain all documentation for at least 5 years

- Review how the claim affected your policy renewal or premiums

- File complaints if necessary with the NJ DOBI

- Consider retaining a public adjuster for future events

In New Jersey, it is legal to reopen claims in certain circumstances—particularly when new damage is discovered or when a claim was wrongly denied or underpaid.

Conclusion

Understanding how insurance claims work in New Jersey can help policyholders protect their rights, document their losses correctly, and avoid unnecessary delays or denials. From initial notification to final payment, each stage of the process presents opportunities—and risks.

While carriers are required to act in good faith, the burden of proof lies with the insured. For many homeowners, professional assistance—whether legal, technical, or adjusting-related—can be essential to achieving a fair result.