If you’re facing pushback or a suspiciously low estimate, here’s how to take control:

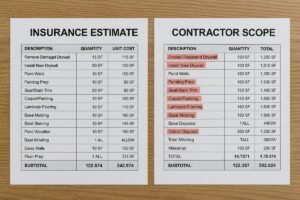

Get a Competing Estimate

Get a Competing Estimate

Have a licensed contractor or public adjuster write a detailed estimate including:

- Full scope of repairs

- Photos and diagrams

- Xactimate or similar pricing

- Code references (if needed)

Demand Justification in Writing

Ask the carrier to explain, in writing:

- Why certain items were excluded

- How pricing was calculated

- Who reviewed the claim and when

This often forces a more careful review.

Submit a Rebuttal with Documentation

Include:

- Photos of all damages

- Expert opinions

- Manufacturer specs or repair standards

- Local material and labor invoices (if available)

Make it harder for the carrier to dismiss your evidence.

Escalate Strategically

You can escalate to:

- A claims supervisor

- The carrier’s internal review board

- The NJ Department of Banking & Insurance (DOBI)

- A licensed public adjuster or attorney

Don’t rely solely on customer service reps—they don’t make payment decision